The Fed: A Hard Landing Cometh

The Fed: A Hard Landing Cometh

"No landing" + sticky inflation is a richly priced stock market's worst nightmare. Look for the S&P 500 to start pricing in a 4Q23-1Q24 "hard landing" scenario in the coming months.

Discussion

Over the course of January The WOTE outlined the case for a US recession starting sometime in 4Q22, but subsequent data has clearly killed that thesis with the January nonfarm payroll report coming in much hotter than expected, and perhaps more importantly, the ISM Services PMI jumping back into expansion territory. In the January 24 “Back to Basics” post The WOTE said:

“Equity market bulls should hope that The WOTE is right. The sooner the US economy contracts and brings inflation back to 2%, the sooner the S&P 500 can move into a new bull market.

“If The WOTE is wrong about the current state of the US economy - as strong equity market breadth, weak defensive sector relative strength, and healthier credit market conditions suggest could be the case - then the Fed will ultimately have to raise rates even more than expected in order to tighten financial conditions enough to contract the economy enough to bring inflation back to 2%.”

What The WOTE described as the alternative case on January 24 was precisely the “no landing” scenario that has now permeated the market conversation. Most importantly for determining how to navigate this scenario, the Fed is in the process of telling us how it will handle it. Over the weekend chief economics correspondent for the Wall Street Journal, Nick Timiraos, wrote about the possibility of a “no landing” scenario. The article hinted that this scenario would mean more Fed rate hikes, but it wasn’t overly specific in just how much more hawkish the Fed would need to become. But on Monday evening Timiraos went on CNBC Overtime to flesh out the details, saying:

“A ‘no landing’ means you don’t get the slowdown in growth that…policymakers at the Federal Reserve have been anticipating. I think a ‘no landing’ scenario is probably just a delayed landing…and the longer you delay this the more likely it probably is that you’re looking at a hard landing.”

“…we’re going to have these questions around how long does this sequence of 25 basis point increases go on for.”

“…if they don’t see the slowdown it means they’re going to take the steps to try to create the slowdown. Whether that means a higher terminal rate or just holding at a higher level for longer, I think that’s what we’re going to find out in the weeks ahead. A ‘no landing’ here is not consistent with what the Fed says they want.”

But it gets worse. Not only is the Fed not getting the economic slowdown it needs, as evidenced by today’s inflation report and subsequent bond market reaction inflation is proving to be far stickier than consensus believed just a few short weeks ago.

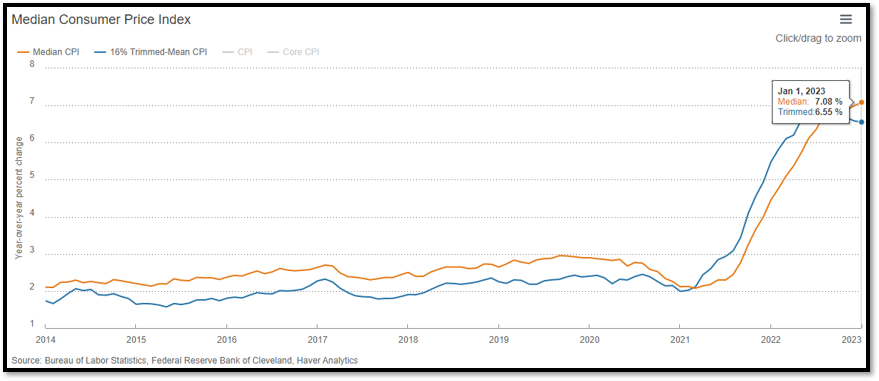

There are many ways to slice the inflation data to get a read on underlying inflation, but the most straight forward is the FRB Cleveland measures of Median and Trimmed Mean CPI. YoY in January 2023 these measures were 7.1% and 6.6% versus 4.5% and 5.5% in January 2022.

Market participants will squint until they’re blind to find the disinflation they so covet in order to get the “Fed pivot” they so desperately need, but the fact of the matter is that above-2% inflation is deeply embedded in the US economy as a result of the “monetary policy 3”1 measures taken in 2020 to combat the COVID lockdowns and requires a stiff economic contraction to bring it back to 2% on a sustained basis.

The highly regarded inflation watcher, Jason Furman, had the following to say on CNBC this morning in response to the hot inflation inflation report:

“I think markets are just ridiculously complacent about the inflation situation right now. I don’t see how we have inflation much below 3% this year. I don’t see it coming down below that without a decent sized recession. And nothing in this number gives me comfort. I think this inflation issue is real, I don’t think it’s going away anytime soon.”

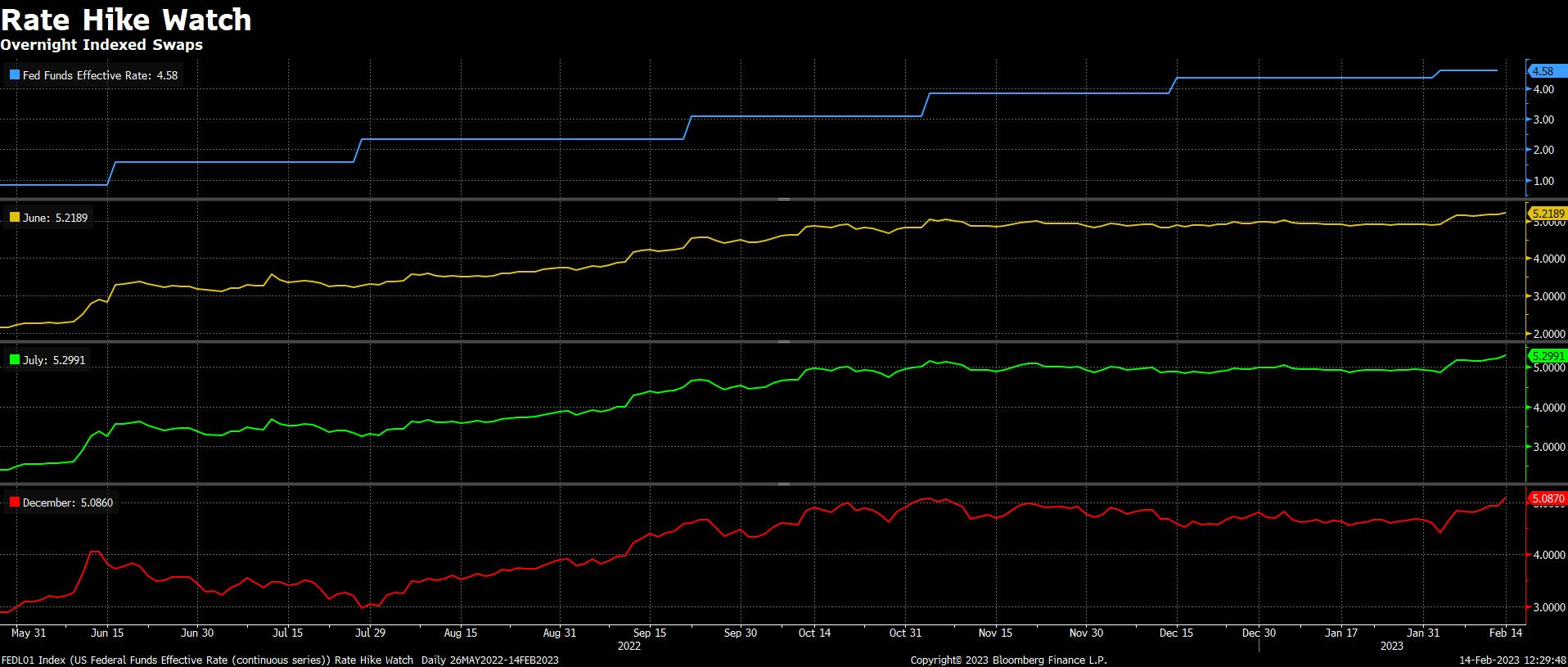

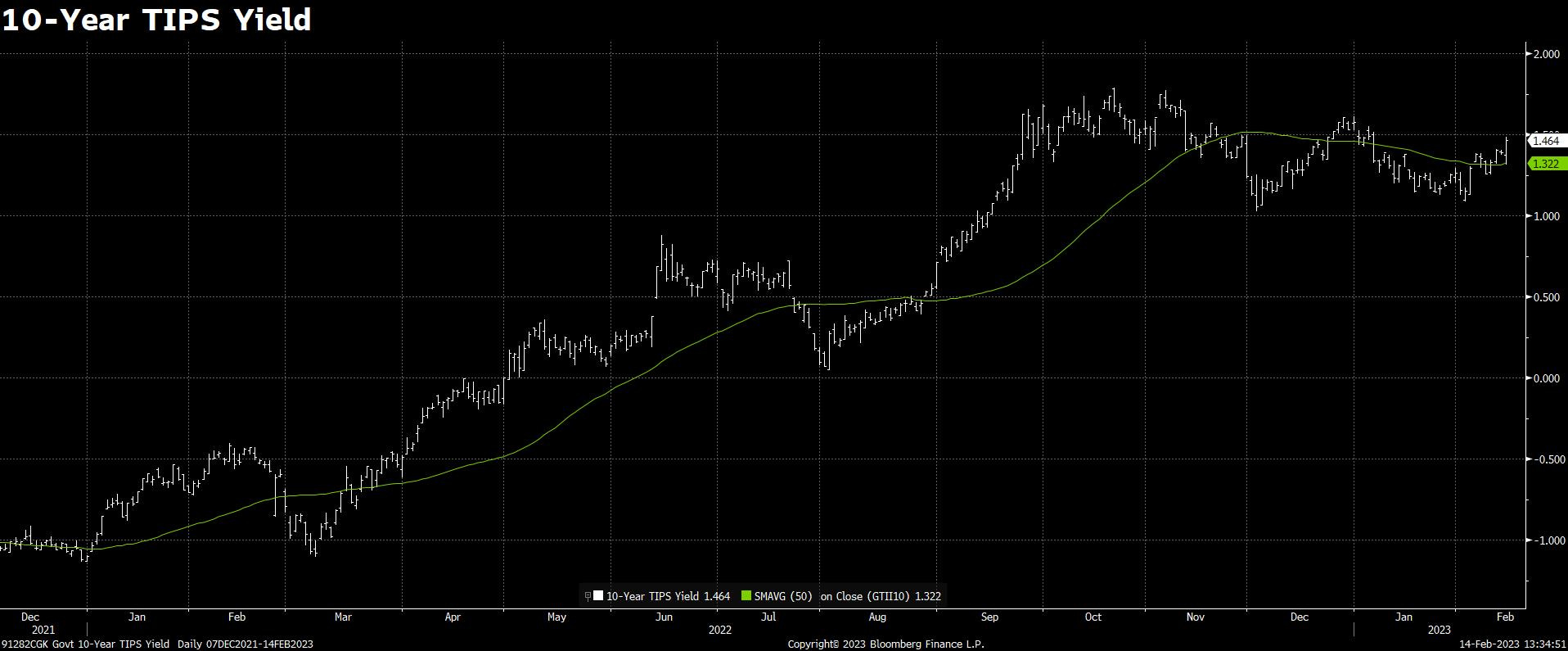

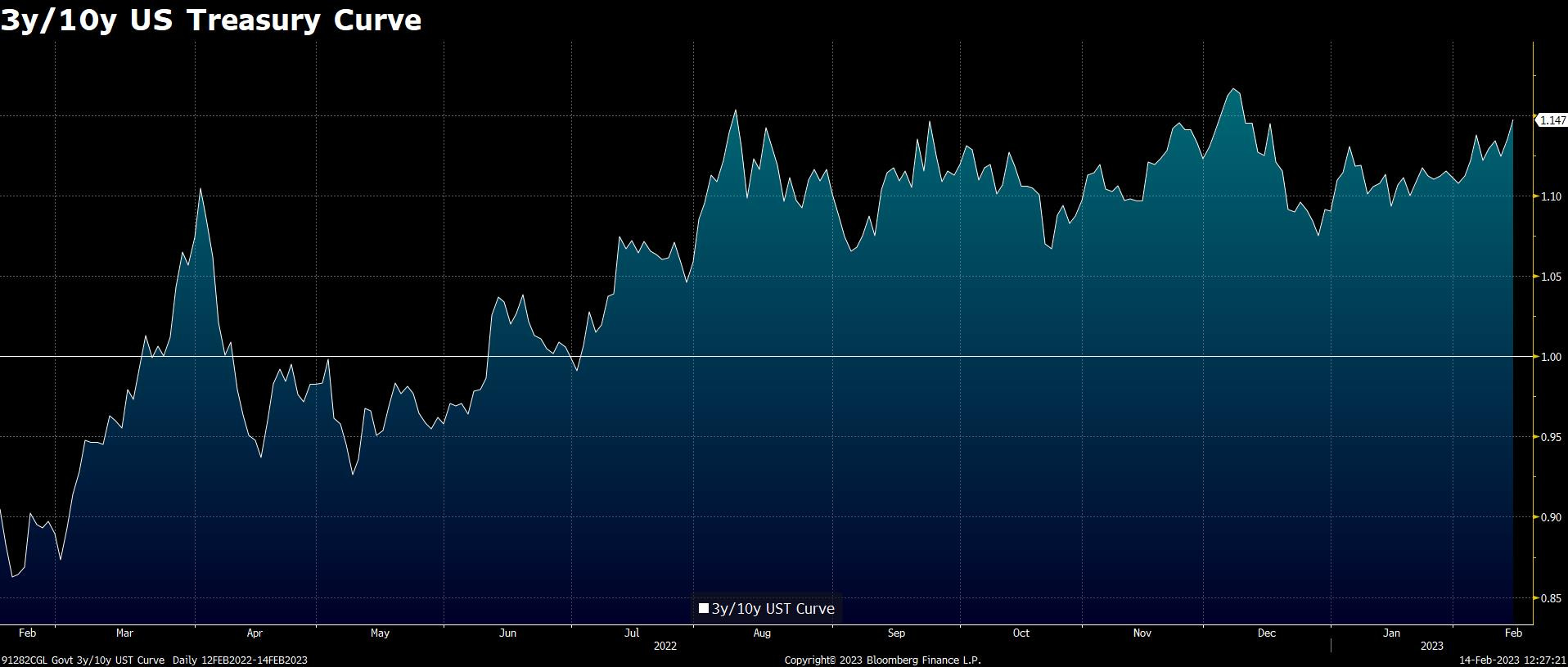

The bond market agrees. The OIS market now has the FFR peaking at 529 bps in July, the 10-year TIPS yield is up to 146 bps, and the 3y/10y US Treasury curve is just under 115%.

“What’s Past is Prologue”

Once Core CPI broke out above 2.5% in the mid-1960s it did not return to 2.5% on a sustained basis until the mid-1990s. Over that time, the “real” 10-year US Treasury yield averaged approximately 280 basis points, as measured by the 10-year yield minus the YoY rate of Core CPI. The WOTE has no idea if that level of real interest rates is required in today’s environment for the Fed to return inflation to 2% on a sustained basis, but it’s a disconcerting thought experiment with the 10-year currently under 400 bps with Core CPI running above 500. Even if the necessary real rate is somewhere around 150, if Core CPI settles out at 400 the 10-year needs to rise to 550 to put sufficient downward pressure on inflation to return it to 2%.

It’s generally thought that the 10-year should peak at around 50 bps below the terminal FFR, so if the Fed needs to get the 10-year to 550 a 600 bps terminal FFR would be required. With the OIS market taking the terminal FFR up to 529 after today’s inflation report, 600 isn’t out of reach, as it would require a 25 bps hike in September, November and December. However…

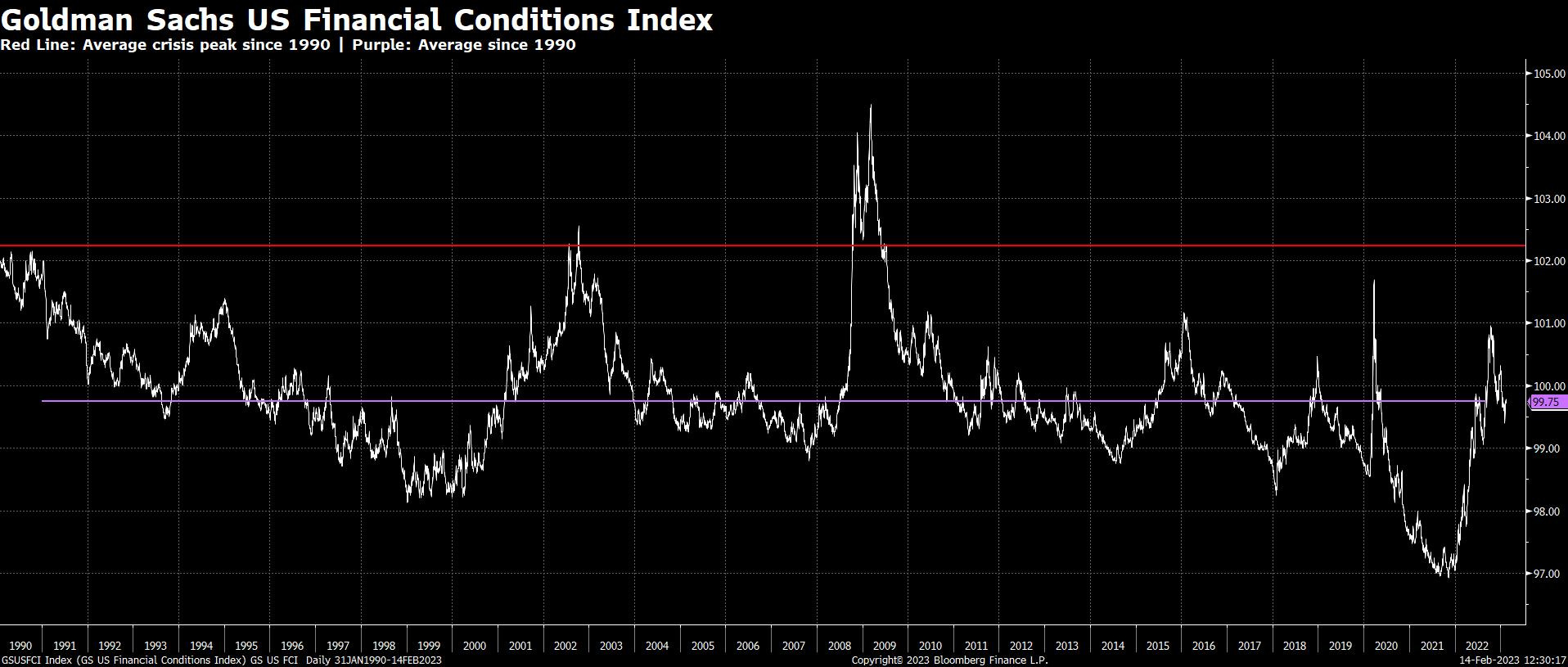

It’s more likely that broader financial conditions do the Fed’s work on its behalf and the Fed never gets to 600, perhaps not even to the currently priced 529. With the S&P 500 priced for perfection, the set-up is there for a dramatic tightening of financial conditions in the coming months that takes the Goldman Sachs US FCI up to new highs, if not to the average level seen in market crises going back to 1990.

Once financial conditions tighten sufficiently, the market conversation will turn to the prospect of a “hard landing” sometime in the 4Q23 to 1Q24 time frame.

A hard landing cometh.